In the international hotel investment market, real strategies are not revealed in press releases. They are revealed in acquisitions.

When an investor buys a hotel, the price paid, the partner selected, the brand chosen, the market entered and the type of risk accepted all say far more than any institutional presentation ever could.

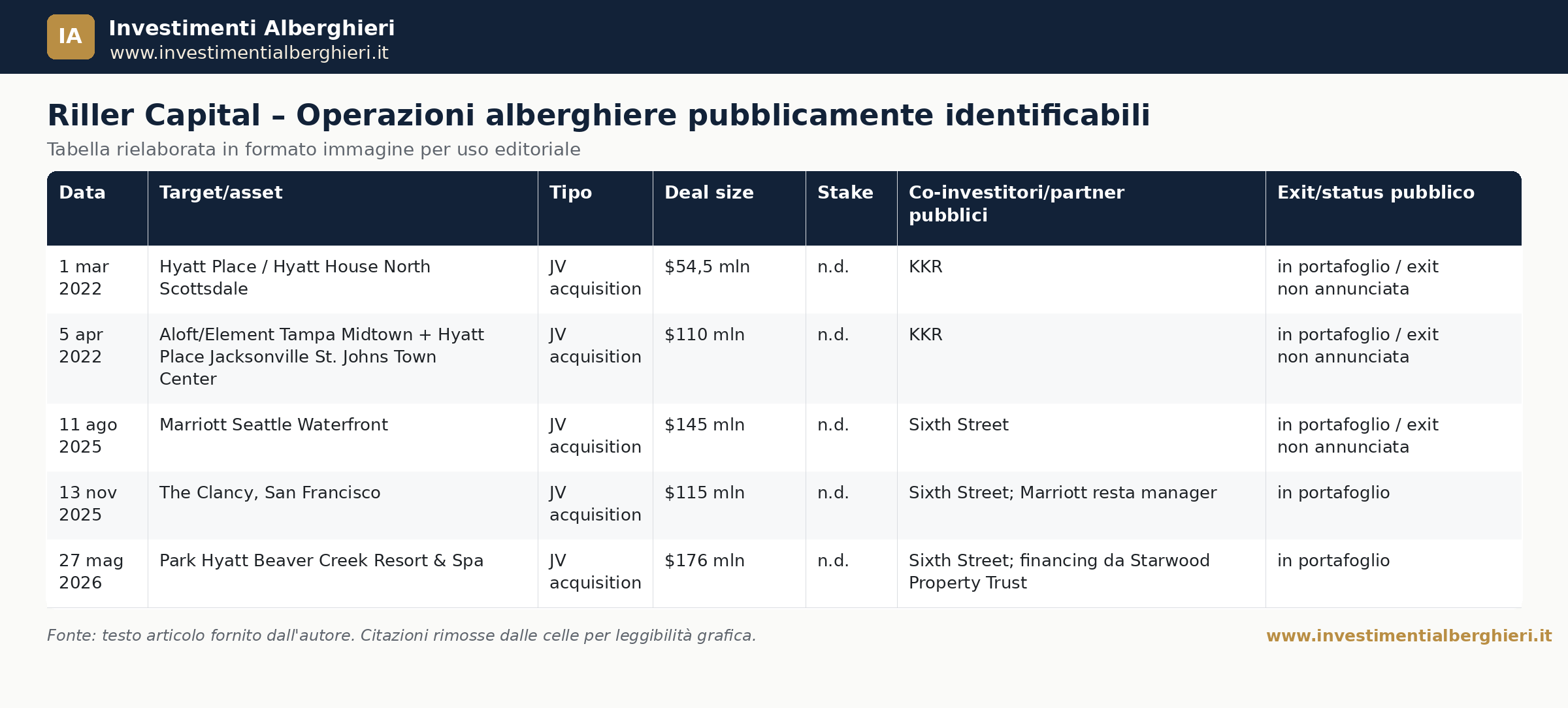

The case of Riller Capital is particularly interesting because it shows the evolution of a hospitality real estate platform: first, select-service and extended-stay acquisitions alongside KKR; then, full-service, lifestyle and luxury resort transactions alongside Sixth Street.

The publicly identifiable transactions analyzed in this article represent approximately $600 million in aggregate deal value and more than 1,500 rooms. Yet the financial figure alone does not explain the broader strategy.

The real point is this: Riller Capital appears to be operating as a hotel investment platform, not merely as a real estate investor.

That distinction is crucial for the Italian market as well, where many hotels are still valued primarily on the basis of the underlying property, the location or the asking price set by the owner. More sophisticated investors, by contrast, analyze a hotel as an operating business embedded within a real estate asset.

That is where value is either created — or destroyed.

For readers seeking to explore these themes further, the Investimenti Alberghieri blog, the hotel guides by Roberto Necciand the updates published on Investhotel provide additional insights into the relationship between management, value creation, investment strategy and hotel asset transformation.

The Publicly Identifiable Hotel Transactions

|

Date

|

Asset

|

Public Partner

|

Deal Value

|

Asset Profile

|

Strategic Reading

|

|---|---|---|---|---|---|

|

March 2022

|

Hyatt Place / Hyatt House North Scottsdale

|

KKR

|

$54.5 million

|

Dual-branded select-service / extended-stay

|

Newer asset, strong brand, high-quality leisure and corporate market

|

|

April 2022

|

Aloft/Element Tampa Midtown + Hyatt Place Jacksonville St. Johns Town Center

|

KKR

|

approx. $110 million

|

Florida select-service / extended-stay portfolio

|

Immediate scale, diversification across two markets, Marriott and Hyatt brands

|

|

August 2025

|

Marriott Seattle Waterfront

|

Sixth Street

|

$145 million

|

Urban waterfront full-service hotel

|

Institutional asset, leisure/corporate/group demand, operational complexity

|

|

November 2025

|

The Clancy, San Francisco

|

Sixth Street

|

$115 million

|

Urban lifestyle hotel

|

Contrarian thesis on San Francisco, urban recovery and convention demand

|

|

May 2026

|

Park Hyatt Beaver Creek Resort & Spa

|

Sixth Street

|

$176 million

|

Luxury ski-in/ski-out resort

|

Trophy asset, product scarcity, high-end leisure demand

|

This table tells a very clear story.

In 2022, Riller Capital appeared in transactions with KKR involving efficient, branded, relatively modern hotels located in markets with diversified demand. In 2025 and 2026, the profile changed: Sixth Street entered the picture, along with more complex full-service, lifestyle and luxury resort assets.

This is not simply an increase in deal size. It is a strategic shift in asset category.

Phase one: Efficient hotels, strong brands and controllable pperating risk

The first two publicly identifiable transactions reveal a highly rational strategy: acquire branded hotels with efficient operating models and locations capable of capturing multiple demand segments.

The acquisition of the Hyatt Place / Hyatt House North Scottsdale for $54.5 million is a classic example of an investment in a newer, dual-branded asset combining transient demand with extended-stay demand.

The logic is clear: a hotel of this kind does not depend on a single demand source. It can attract business travelers, leisure guests, short-stay customers and longer-stay guests. The dual-brand structure also allows the property to serve complementary segments, potentially improving occupancy stability.

The second transaction, the portfolio comprising Aloft/Element Tampa Midtown and Hyatt Place Jacksonville St. Johns Town Center, reinforces the same approach. In this case, the acquisition was not of a single hotel, but of a critical mass spread across two Florida markets.

Here again, the brands matter. Aloft captures a more lifestyle-oriented urban demand profile. Element serves the extended-stay segment. Hyatt Place offers a solid and recognizable select-service model. The result is a portfolio that is easier for institutional capital to understand and potentially more efficient to manage.

This first phase suggests an important principle: for a hotel investor, a brand is not merely a commercial sign above the door; it is a risk-reduction tool.

A brand supports distribution, strengthens visibility, facilitates financing and makes the asset more understandable to banks, partners and future buyers. But the brand alone is not enough. It must sit within a coherent economic structure.

Phase two: more complex assets, greater ambition and deeper value creation

The second phase is far more interesting from an industrial and operational perspective.

With the Marriott Seattle Waterfront, Riller Capital, together with Sixth Street, entered a $145 million urban full-service transaction. The asset benefits from a waterfront location, meaningful scale and potential demand from leisure, corporate, group, event and meeting segments.

Here, complexity increases substantially. A full-service hotel cannot be managed like a select-service property. It has more departments, higher costs, more ancillary revenue opportunities, greater capital expenditure requirements, more brand standards, higher operating risk and more ways to either create or lose value.

That complexity is precisely what makes the transaction interesting.

A purely real estate investor might analyze this type of hotel primarily through price, location and cap rate. A hospitality-specialized investor, however, will also examine distribution, meeting space, food and beverage, payroll, reputation, customer mix, contracts, capital expenditure and repositioning potential.

The difference is substantial.

A well-governed full-service hotel can create value through operating levers that are not immediately visible in a conventional real estate valuation. Conversely, if poorly managed, it can erode profitability despite a strong location.

The Clancy: The most contrarian bet

Among the transactions analyzed, The Clancy in San Francisco is arguably the most interesting from a risk perspective.

San Francisco has been one of the most debated urban hotel markets in the United States in recent years. The slowdown in corporate travel, challenges in the downtown area, perceptions around safety and the post-pandemic transformation of demand have all affected the performance of many urban hotels.

Acquiring a 410-room lifestyle hotel in this context is not a simple, low-risk decision.

It is an investment thesis.

The buyer of The Clancy is not merely acquiring rooms, a restaurant, meeting spaces and a brand. It is buying into a conviction: that San Francisco can recover its attractiveness, convention demand, urban tourism and corporate flows, also supported by the renewed centrality of innovative sectors such as technology and artificial intelligence.

This type of transaction is particularly instructive for the Italian market.

Italy also has assets located in strong destinations that may be temporarily penalized by weak management, unclear positioning, excessive debt, deferred capex or inconsistent contracts. A sophisticated investor does not look only at the problem. A sophisticated investor looks at the possibility of turning that problem into return.

Naturally, the risk remains significant. But in the hotel sector, return often comes from the ability to identify an inflection point before the rest of the market does.

Park Hyatt Beaver Creek: When value lies in scarcity

The acquisition of the Park Hyatt Beaver Creek Resort & Spa represents the qualitative peak of the transactions analyzed.

This is not an urban hotel requiring repositioning. It is a luxury resort in an alpine destination with high barriers to entry. The $176 million price, equivalent to more than $900,000 per room, immediately signals one thing: the market is not valuing only the current income statement, but the scarcity of the product.

A ski-in/ski-out resort in a destination such as Beaver Creek cannot be easily replicated. The combination of the Park Hyatt brand, direct mountain access, high-end leisure demand, resort services, spa, food and beverage, events and multiple seasonal demand drivers creates a profile that is fundamentally different from a standard urban hotel.

This transaction highlights a second major lesson: hotel assets are not all equal because their substitutability is not equal.

A standardized hotel in a highly competitive market may face pricing and margin pressure. A luxury asset in a location with limited supply may maintain stronger pricing power, particularly when demand comes from high-spending, less price-sensitive guests.

For an investor, this means that price per room must always be interpreted within context. A high value is not necessarily evidence of overpricing. It may reflect genuine scarcity, a strong brand and the ability to generate long-term income.

The real issue: Riller Capital is not buying hotels, it is buying business plans

The most interesting reading of these five transactions is that Riller Capital does not appear to be acting according to a generic opportunistic logic.

It is not simply buying “hotels”.

It is buying business plans.

In the case of select-service assets, the business plan may revolve around efficiency, stabilization, demand growth and disciplined cost management.

In the case of the Marriott Seattle Waterfront, the thesis involves an urban full-service asset with diversified demand and potential value creation through management and positioning.

In the case of The Clancy, the business plan is tied to the recovery of a complex market.

In the case of the Park Hyatt Beaver Creek, value lies in scarcity, quality and the ability to maintain pricing power in the luxury segment.

This is the difference between a real estate approach and a hotel investment approach.

The real estate approach starts with the asset.

The hotel investment approach starts with demand, management, profitability and transformation potential.

Five lessons for hotel investors in italy

1. Price per room is not enough

Price per room is a useful indicator, but it can be misleading when read in isolation. A hotel priced at €300,000 per room can be either expensive or attractive depending on profitability, required capex, management quality, destination strength and contractual structure.

In the Italian market, where many hotels are still presented using values based on square meters, location or ownership expectations, a methodological shift is required. The key question should not only be “How much does it cost?” but “How much sustainable income can it generate?”

2. Governance matters as much as location

Location remains fundamental, but it is no longer sufficient. A hotel in an excellent location, if poorly managed, can underperform a less central asset governed with discipline and method.

Management control, revenue management, distribution channels, brand positioning, maintenance, online reputation and managerial quality all have a direct impact on value.

This is why the hotel guides by Roberto Necci are useful for those who want to understand not only the real estate component of a hotel, but also its operating and managerial dimension.

3. Institutional capital requires readable numbers

Funds, banks, family offices and professional investors do not buy generic narratives. They buy verifiable numbers.

A hotel without orderly reporting, reliable historical data, a credible business plan, clear contracts and mapped capital expenditure is perceived as riskier. And in the capital markets, risk almost always translates into a discount on price.

This is one of the major structural weaknesses of the Italian market: many interesting assets are not investment-ready.

4. The brand helps, but it does not replace management

The transactions analyzed involve strong brands: Hyatt, Marriott, Aloft, Element and Park Hyatt. But a brand is not an automatic guarantee of success.

A brand brings distribution, standards, visibility and trust. However, if the product is weak, costs are out of control or management is inadequate, even a major brand may not be enough.

In hospitality, value is created through the balance between brand, management, product, market and capital.

5. A hotel is a business, not a passive real estate asset

This is the most important lesson.

A hotel is not an office leased to a tenant, a retail unit under a long-term contract or an apartment generating passive rental income. It is a daily operating business exposed to demand, pricing, reviews, labor, technology, distribution, competition and economic cycles.

Investors who enter the hotel sector without understanding its operating nature risk underestimating the true level of risk.

Those who understand it can identify exceptional opportunities.

What this means for hotel owners and operators

The Riller Capital case does not concern only private equity funds, international investors and large U.S. transactions. It also concerns Italian hotel owners and operators.

The message is very practical: a well-governed hotel is worth more.

It is worth more when it is sold.

It is worth more when it seeks financing.

It is worth more when it looks for an industrial partner.

It is worth more during generational transition.

It is worth more when it needs to be repositioned.

Many hotel entrepreneurs focus on revenue, but the market is increasingly looking at the quality of earnings. It is no longer enough to say that the hotel performs well. Owners must demonstrate how it performs, with what margins, with what customer mix, with what risks, with what prospects and with what management structure.

This is the decisive cultural shift.

A hotel should not merely be operated. It must be made legible.

The italian challenge: many interesting assets, few assets ready for capital

Italy has an extraordinary hotel heritage. Art cities, leisure destinations, lakes, coastlines, historic towns, mountain resorts and corporate markets offer opportunities that few countries can match.

But there is a structural issue: many hotels are not prepared to engage with professional capital.

Solid business plans, management reporting, capex analysis, segmented data, market benchmarks, repositioning plans, coherent contracts and a clear vision of future governance are often missing.

This does not mean that these assets lack value. It means that their value is not fully expressed.

A hotel can have enormous potential and still be perceived as risky if it is not presented correctly.

This is where advisory, asset management and hotel-specific expertise become essential.

Why buying well is not enough

One of the most dangerous misconceptions in hotel investment is the idea that success depends only on the acquisition price.

Buying well matters, but it is not enough.

In the hotel sector, value is created after the acquisition: through staff management, pricing strategy, distribution, contracts, cost control, maintenance, reputation, brand relationship and the ability to read the market before competitors do.

The Riller Capital transactions demonstrate exactly this. Financial capital is fundamental, but capital alone does not create hotel value. A platform of expertise is required.

You need to know what to analyze before the acquisition.

You need to know what to change after the acquisition.

You need to know when to invest, when to wait and when to sell.

That is the difference between buying a hotel and creating value in hospitality.

A reading for italian investors

For an Italian investor, the Riller Capital case offers three practical indications.

The first is that the hotel market must be analyzed by segment. A select-service hotel, an urban lifestyle property and a luxury resort cannot be valued through the same lens.

The second is that the partner matters. The transactions with KKR and Sixth Street show that institutional capital prefers to work with specialized platforms capable of translating hotel risk into an actionable plan.

The third is that value is not static. A hotel can become more valuable if it is repositioned, if distribution improves, if management changes, if costs are optimized, if it captures new demand or if it becomes part of a broader platform.

This is particularly relevant in Italy, where many potential transactions fail to move forward because there is no professional reading of the asset. The problem is not always the price. Often, it is the absence of a clear investment thesis.

Conclusion: The Future of hotel investment will be selective

The Riller Capital transactions point to an increasingly evident trend: capital continues to look at hotels with interest, but it does so selectively.

Not all hotels are investable.

Not all assets are financeable.

Not all operating models are value-enhancing.

The future of hotel investment will reward operators and investors capable of combining capital, management, data, governance and strategic vision.

For the Italian market, this is a major opportunity. Hotels with strong locations, unexpressed potential and room for operational improvement can become highly attractive assets. But they need to be analyzed, structured and presented with discipline.

The issue is not merely buying or selling a hotel.

The real issue is understanding what value that hotel can express if it is properly governed.

To continue exploring case studies, metrics, valuations and strategies in hospitality, visit the Investimenti Alberghieri blog, the hotel guides by Roberto Necci and the updates published on Investhotel.

Do you want to understand the real potential of your hotel?

Are you considering the acquisition, sale, repositioning or value enhancement of a hotel?

Before submitting an offer, opening a negotiation, seeking financing or launching a turnaround plan, you need a professional reading of the asset: numbers, management, contracts, capex, positioning, demand, margins and real potential.

Hotel Management Group supports owners, investors and operators in the governance, advisory and value enhancement of hotel assets, with an integrated approach focused on profitability, economic sustainability and long-term value creation.

Request a strategic consultation at hotelmanagementgroup.it.

Roberto Necci - r.necci@robertonecci.it